Default On Private Student Loan – Media Domino: A Blog About Student Loans How Private Student Loans Deepen Racism in the Student Loan Market

About 45 million borrowers nationwide have student loan debt totaling $1.7 trillion, including more than $140 billion in private student loan debt. Private student loans provided by banks and other private lenders are playing an increasingly important role in the student loan market without federal government intervention, contributing to the student debt crisis. mortgage The private student loan market grew rapidly in the years following the Great Recession, following the growth of the auto loan and credit card markets. Despite industry assurances that the private student loan market is immune from borrower distress, A closer examination of the results confirms that some borrowers are suffering disproportionately from private student loan debt: Black and Latino borrowers.

Contents

- Default On Private Student Loan

- Student Loan Defense To Repayment

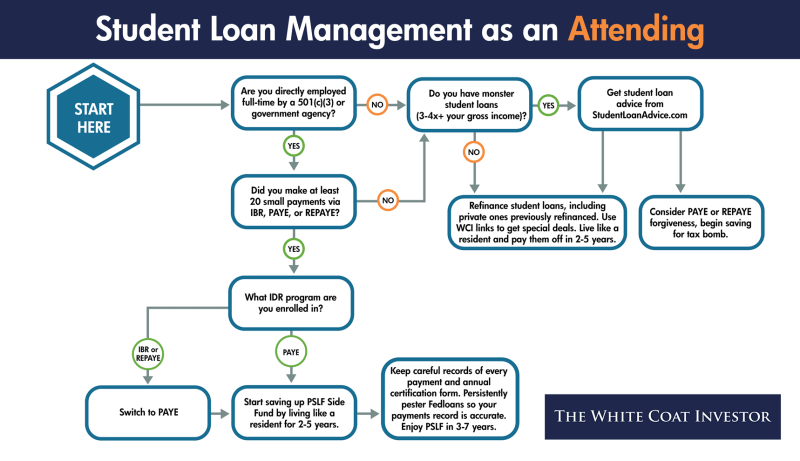

- Exposing The Student Loan Racket (infographic)

- Best Private Student Loans Companies For 2023

- How I Recovered From A Student Loan Default And Rebuilt My Credit

- Student Loan Pause Has Benefitted Affluent Borrowers The Most, Others May Struggle When Payments Resume

- Social Security Benefits Can Be Taken To Pay Student Loans In Default

Default On Private Student Loan

This disparity is particularly acute in the private student loan market. Black students are half as likely to get private student loans, but four times more likely than their white peers to have trouble repaying private student loans. This disparity is particularly significant because private student loans pose additional risks for borrowers. Unlike federal student loans, Private student loans have few protections to mitigate default when borrowers experience financial hardship. Since the default relief arrangements are left to the discretion of the borrowers; Struggling borrowers have few options to seek help if they fall behind.

Student Loan Defense To Repayment

In addition, Students attending for-profit institutions are more likely to use expensive private student loans to finance their education. This includes unregulated shadow student debt—debts that are often exploited without substantial oversight and for-profit institutions that target students and loan products. school. The main features of these products are high interest rates; Includes misleading marketing and risky insurance schemes. Because black students are overrepresented at these institutions; The harm caused by this abusive debt falls disproportionately on the black community.

The burden of the student debt crisis is not borne equally. Black and Latino borrowers suffer some of the worst consequences related to this debt, beginning with the systemic discrimination that permeates our nation’s financial markets. Exclusive economic policies and racial discrimination have led to racial wealth disparities where the median white household is 13 times richer than the median black household and 10 times richer than the median Latino household. So even though the average white student loan borrower repays almost 95% of their loans within 20 years of starting college.

After a similar period, This is 95% of the original balance. Debt-based higher education only reinforces and exacerbates these systemic barriers, and a closer look at differences in borrower performance in the private student loan market reveals similar trends.

The transparency of the private student loan market results in different loan outcomes; It only adds to concerns about repayment difficulties and the ruthless targeting of black borrowers. Little information is available about the private student loan market and borrower outcomes. That’s in part because the Trump administration’s Consumer Financial Protection Bureau abandoned a 2017 effort to finally collect comprehensive information from companies operating here. With this in mind, The racial disparity seen in the market from the limited statistics currently available has prompted regulators to tighten oversight of private student lenders for practices that may have a disparate impact on black borrowers. In the absence of strict CFPB oversight. States can continue to fill this gap by passing new independent oversight and state-level protections.

Exposing The Student Loan Racket (infographic)

The student debt problem is a civil rights crisis. As policymakers seek to improve economic mobility for vulnerable communities, it is important to take steps to address the role of private student loans in exacerbating financial hardship and wealth inequality. The private student loan market and for-profit private repayment results call for stronger protections for private student borrowers, with private student loans targeting black borrowers.

Lenders need proactive protections from harmful practices in the private student loan market that exacerbate systemic racial barriers within Black and Latino communities. Higher education should open the door to economic mobility, not debt-ridden borrowers that further entrench racial inequality.

Kat Welbeck is a civil rights attorney at the Student Borrower Advocacy Center. She was previously an outreach and engagement specialist in the CFPB’s Office of Public Engagement and Community Liaison. The government supports federal student loans after students or their families complete the FAFSA. These terms are mandated by law and include certain protections that do not apply to personal loans, such as fixed interest rates and income-based repayment plans. Unlike federal loans, private loans come from private companies such as banks or credit unions. Personal loans have terms and conditions set by the lender. Private student loans are generally more expensive and have fewer benefits and protections than federal student loans.

Federal student loan information is available at www.StudentAid.gov. If you can’t find loan information on StudentAid.gov without knowing the name of your lender or servicer. You most likely have a private loan. You can find information about your personal loans by checking your credit report.

Best Private Student Loans Companies For 2023

All student loan information displayed in your www.StudentAid.gov account is for federal loans. It is common for lenders to have both federal and private loans. If you have a loan that does not appear on your www.StudentAid.gov account, It is important to check your credit report to find out who your personal loan company is.

Federal loans have lower fixed interest rates than private loans. Private student loans can have variable or fixed interest rates. Private student loan interest rates can be higher or lower than federal loan rates.

Only federal student loans are eligible for a government repayment plan. If you have personal student loans and are struggling to make your monthly payments, You should contact your loan servicer and ask about the repayment plans they offer. As of December 2019, approximately 43 million Americans held federal student loans, and with borrowers struggling to make repayments, the education finance system is under pressure exacerbated by the complexity of the repayment process.

U.S. According to the Department of Education, about 20% of borrowers are in default (generally defined as not making payments for at least 270 days), and more than one million loans go into default each year.

How I Recovered From A Student Loan Default And Rebuilt My Credit

A recent study found that while many borrowers keep their loans current, some borrowers default multiple times. Of those who returned their loans to good standing, 25% defaulted again within five years.

Most federal student loans are serviced by third-party servicers that contract with the Department of Education. The company’s operations include collecting payments and helping borrowers access tools to choose repayment plans and pause payments. After the borrower defaults, The servicer often refers the loan to a private collection agency, which typically refers it to the Department of Education.

Failure to repay student loans can have serious financial consequences for the borrower, including collection fees. decoration fee; income tax refunds; amounts withheld from Social Security and other federal payments; damaged credit score; You may not qualify for other assistance programs, such as homeowner’s assistance. These consequences can also affect the financial security of the family.

Defaulting borrowers face all sorts of dire consequences. Loss of access to repayment tools and other federal programs.

Student Loan Pause Has Benefitted Affluent Borrowers The Most, Others May Struggle When Payments Resume

Interest continues to accrue on the loan even if the borrower defaults. In addition, Borrowers who enroll in monthly payment plans that match borrower income and family size will not be able to default on loan forgiveness programs and benefits for 20 to 25 years after qualifying payments. . . and defaulted borrowers are not eligible for additional federal student aid.

While interest continues to accrue, the Department and collection agencies may charge defaulters up to 25% of principal and interest. U.S. Treasury deductions, known as offsets, related to fees that government agencies and debt collectors charge. Borrower’s social security; Federal income tax refunds or other federal payments (see refunds below for details).

Servicers are required to report loans more than 90 days delinquent to the regular state credit bureaus. These notes remain on the borrower’s credit report for up to seven years.

Studies show that, on average, a student loan borrower’s credit score drops 50 to 90 points during student loan default; It is possible due to late payments, and the borrowers who fail to pay their student loans are behind other bills. The individual credit scores may immediately recover after failure. Debt borrowers can end up paying more or the struggles.

Social Security Benefits Can Be Taken To Pay Student Loans In Default

Can you default on private student loans, student loan default lawyer, private student loan default settlement, student loan default, private student loan default options, student loan default forgiveness, private student loan default help, private student loan default rate, student loan default rehabilitation, private student loan default consequences, student loan default help, private student loan default